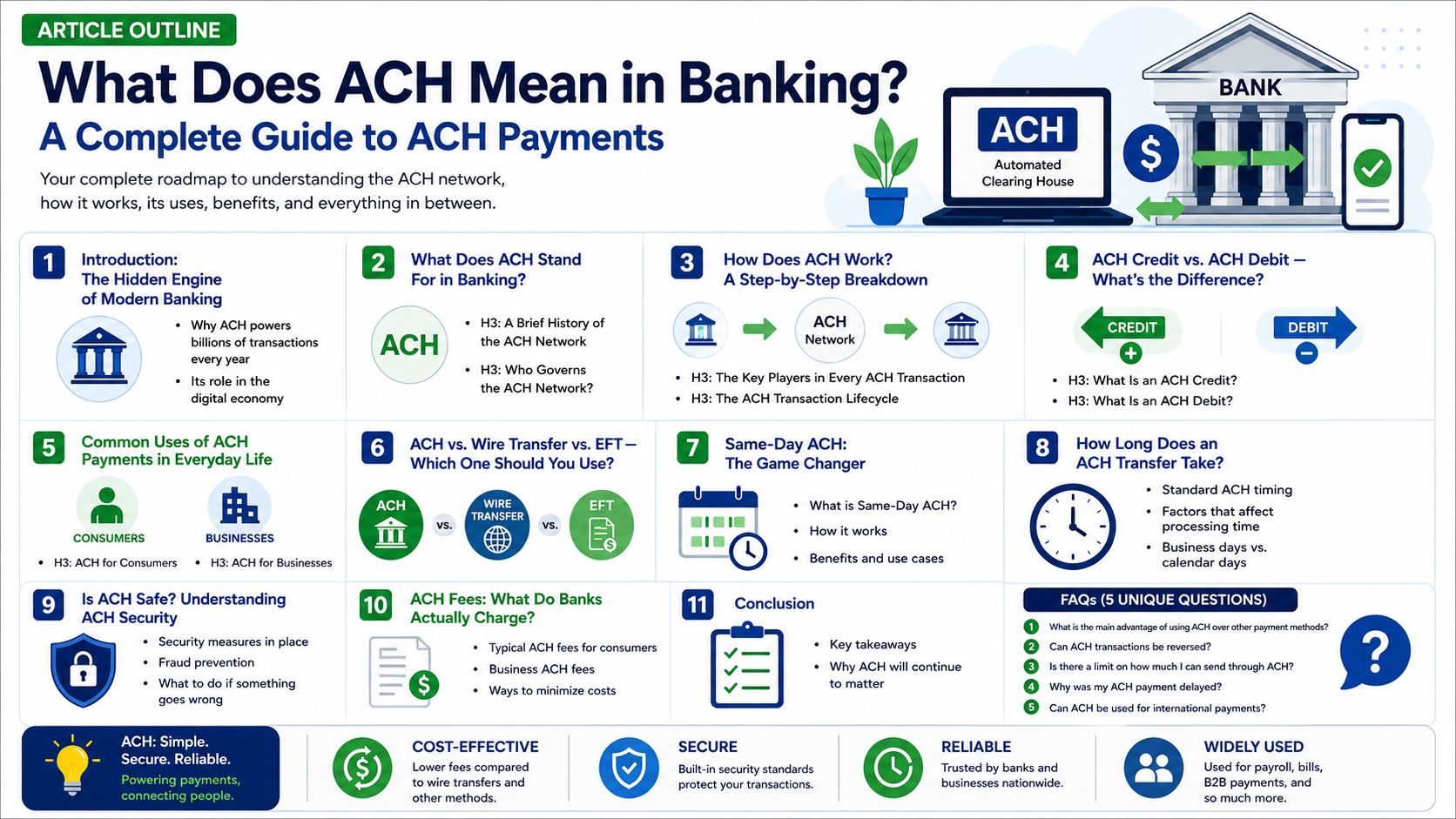

Table of Contents

What Does ACH Mean in Banking? A Complete Guide to ACH Payments

The Hidden Engine of Modern Banking

You might have looked at your bank statement. Seen the letters “ACH” next to a transaction and had no idea what it meant. You are not the one. The ACH system is used by millions of people every day. They do not even realize it because it works so quietly and efficiently behind the scenes. The ACH system is like the pipes under your life. You do not see them, but without them, everything would get messed up really fast. Whether you are getting your paycheck deposited on a Friday morning or paying your bill online or sending rent money to your landlord, the Automated Clearing House is probably doing the hard work for you.

The size of the ACH system is really amazing. The number of payments made through the ACH Network went up by 6.7 percent from 2023 to 2024. It reached 33.6 billion payments. The total value of these payments was 86.2 trillion dollars, which is 7.6 percent more than the year before. That is a lot of money. Most people in the United States do not know what the ACH system is, even if you offered them money to explain it. This guide is going to teach you about the ACH system. By the time you finish reading, you will know what the ACH system means, how the ACH system works, and why the ACH system is important. You will also learn how to use the ACH system to help you with your business finances and how the ACH system can help you with your money. Square

What Does ACH Stand For in Banking?

The Automated Clearing House, or ACH, is a system that helps people move money around. ACH is like a network that lets people make payments and transfer money electronically. This network is used in the United States. It is really good for moving money between banks and other places that deal with money.

The good thing about the Automated Clearing House is that you do not need to use cash or write checks to move money. You also do not need to use credit cards or do wire transfers. An automated clearinghouse is like a computer system that helps money get from one bank account to another bank account. It does this in a safe and reliable way. The Automated Clearing House network can even handle money transfers between thousands of banks and financial institutions all at the same time. Simple Fast Loans

ACH is a network that facilitates electronic money transfers and automatic payments between more than 10,000 banks and financial institutions. Some of the most popular ACH payments include direct deposits, paychecks, tax refunds and bill payments. The power of ACH lies in the fact that it can be used by virtually every financial institution in the country. Whether your bank is a giant like Chase or a small local credit union, the ACH network ties them all together under one electronic umbrella. That means you can move money from one to the other without anyone having to physically shuffle a single dollar bill. SmartAsset

A Brief History of the ACH Network

To really understand what ACH does, it helps to understand where it came from. California’s first ACH association was founded in 1972 to process electronic payments and, two years later, NACHA was chartered to run the ACH Network. Before ACH there were stacks of paper checks for payroll and mailing envelopes with physical money inside for bill payment. The introduction of a centralized electronic clearing system in the 1970s was revolutionary. It was the financial equivalent of moving from horse-drawn carriages to automobiles. In the ensuing half century, ACH went from a niche tool for large institutional payments to the backbone of everyday consumer banking in the United States.. Simple Fast Loans

The ACH network was initially used mainly for processing recurring payments, but now is widely used for processing one-time debit transfers, such as converted check payments and telephone and Internet payments. This shift from repetitive to one-time payments created an entirely new universe of opportunities for consumers and businesses alike, cementing ACH as the country’s leading electronic payment rail. Federal Reserve

Who Governs the ACH Network?

The ACH network is maintained by the National Automated Clearing House Association (Nacha), a standalone organization owned by a consortium of banks, credit unions, and payment processing companies. Nacha establishes operating rules, security standards and compliance requirements for all participants. Nacha is like the umpire in a giant game of money . It doesn ’ t process the payments itself , but it makes sure everyone ’ s playing by the same rules . There are two ACH operators: the public FedACH and the privately operated Electronic Payments Network (EPN). If the ODFI and the RDFI use different operators, the first operator will transfer the transaction to the second operator. The two-operator model gives redundancy and competition, helping to keep costs low and reliability high across the network. StripeSmartAsset

How Does ACH Work? A Step-by-Step Breakdown

Now that we know what ACH is, let’s pull back the curtain and see how it really works. The process is more elegant than you think. At a high level ACH is like a giant sorting office – payments come in from thousands of different banks, get sorted and batched and then go back out to the correct destination banks. It’s a system designed for efficiency and that’s why it can process more than 33 billion transactions a year without breaking a sweat.

The Key Players in Every ACH Transaction

Each ACH transfer has a cast of characters, each with a role to fill. The Originating Depository Financial Institution ( ODFI ) is the bank that sends the ACH transfer request . Receiving Depository Financial Institution (RDFI): The bank that receives the ACH request. Between the two institutions is the ACH operator, either FedACH or the Electronic Payments Network, the central processor that routes payments between banks. The person or business making the payment is the originator and the person or business receiving the payment is the receiver. Whether you’re setting up a direct deposit or paying a bill online, you’re the sender or receiver in an ACH transaction. Stripe

The ACH Transaction Lifecycle

So what really happens when you click the “Pay” button and the money ends up in someone else’s account? The bank that sends the money, which is called the ODFI, will ask the bank that receives the money, which is called the RDFI, to move the funds. The two banks talk to each other to make sure there is money in the account that is sending the money. If there is money, then the transfer can happen. At this point the ODFI makes a file with all the information about the transfer, like the account numbers and how much money is being moved. This file gets put together with a lot of transactions and sent to the company that helps move the money, which is called the ACH operator. The ACH operator sorts everything out. Sends it to the right banks. The ACH network does this four times a day. It takes all the transactions, sorts them out, and puts them into groups to send to each bank that receives the money, which is called the RDFI. The money transfer system is well organized. It is efficient. Can handle a lot of transactions. It is also pretty fast, which is surprising because it has to handle many transactions. The ACH network and the banks, like the ODFI and the RDFI, work together to make sure the money gets to where it needs to go. StripePlaid

ACH Credit vs. ACH Debit — What’s the Difference?

The concept of ACH is something that you need to understand and one of the things about ACH is knowing what is an ACH credit and what is an ACH credit versus an ACH debit. ACH credits and ACH debits are terms that people get mixed up because ACH credits and ACH debits are used in a way when you are, at the bank compared to when you are just talking to someone. If you know what ACH credits and ACH debits are then you will be able to understand your bank statements. You will not get confused when you are setting up payments that are automatic and use ACH credits and ACH debits.

What Is an ACH Credit?

When someone wants to send money from their account to someone’s account, they use the ACH network to do this. This is called an ACH credit payment. For example, an employer will use the ACH network to send payroll to their employees. The government also uses the ACH network to send cash payments to people who’re eligible.

An ACH credit payment is like a message that says, “Take my money and give it to this person.” When you get your paycheck directly into your account, this is an example of an ACH credit payment. The same thing happens when the IRS sends you a tax refund electronically.

You can think of an ACH credit payment like money being sent to you. A lot of people get paid using ACH credit payments, which are also known as deposits. In fact, a high percentage of Americans, 92%, get paid using ACH credit payments. This shows how common ACH credit payments are in America. ACH credit payments are a part of how money is moved around in America. PlaidPlaid

What Is an ACH Debit?

An ACH debit is the opposite of payments. It does not send money out; it takes money from your account. This is what happens with ACH debit transactions. They take money from your account. For example, you can set up payments for your bills. You can tell your mortgage lender or the company that sends you electricity or your streaming service to take money from your checking account every month. When you do this, you are using an ACH debit. This is an easy way to pay your bills that happen every month. You do not have to remember to pay them because the money is taken automatically. You have to be careful with ACH debits. You need to make sure you have money in your account. If you do not have money, the payment will not go through. This is called a bounced payment. If this happens, you might have to pay fees. Your bank will charge you, and the company you were trying to pay will also charge you. So it is an idea to have some extra money in your account. This way you can avoid these fees. Everything will go smoothly with your ACH debit transactions and your ACH debit payments. SquareConsumer Financial Protection Bureau

Common Uses of ACH Payments in Everyday Life

ACH is not a complicated banking term. It is a part of life for most Americans when managing their money. You might be surprised at how many financial activities you already do through the ACH network. You use ACH more often than you think. It is used for daily financial tasks.

ACH for Consumers

For the person, ACH is a part of almost every financial thing they do. When you get your salary, social security benefits, and tax refunds into your account that is ACH at work. These are examples of ACH credit transfers. On the other hand, ACH debit transfers happen when you pay for things like mortgages and utility bills directly from your account. Ach does more than just those big things. ACH also helps people send money to each other using apps like Venmo or Cash App. When you move money from one of these apps to your bank account, it goes through the ACH network. You can also use ACH when you pay bills online through your bank. You just have to enter the biller’s information and schedule the payment. Many businesses let you pay them using ACH too. To do this, you give them your account number and bank routing number. These two numbers are like your ACH address. If you share them with someone you trust, like a biller, you can pay them electronically using ACH. Federal ReserveConsumer Financial Protection Bureau

ACH for Businesses

For businesses, ACH is a big deal. Businesses that use ACH payments usually pay 40 percent less in fees compared to using credit cards. When you think about how transactions businesses do, the money they save is huge. ACH direct debit lets businesses take payments from customers’ bank accounts. This way of paying is used for things like subscription services, insurance, loan payments, and other bills. It helps businesses know how much money is coming in and saves them money on fees compared to using credit cards. For businesses that work with businesses, ACH is a popular choice. In 2024, 7.3 billion payments between businesses were made using ACH. ACH is great for businesses because it lets them pay vendors automatically, handle payroll for a lot of employees, and collect subscription fees without paying credit card fees. This is why ACH payments are the choice of businesses that want to run. Plaid + 2

ACH vs. Wire Transfer vs. EFT — Which One Should You Use?

If you have ever sent money electronically, you have probably seen a few options and thought about which Electronic Fund Transfer option is the best choice for you. Let us look at the differences between ACH payments, wire transfers, and electronic fund transfers so you can make a good decision every time you need to send money electronically with ACH or electronic fund transfers or wire transfers.

| Feature | ACH Transfer | Wire Transfer | EFT (General) |

|---|---|---|---|

| Speed | 1–3 business days | Same day (often hours) | Varies by type |

| Cost | Very low or free | $10–$60 per transfer | Varies |

| Reversibility | Yes (within limits) | Rarely reversible | Varies |

| Best For | Recurring payments, payroll | Large, urgent transfers | Broad category |

| Processing | Batched (3x daily) | Real-time | Varies |

Wire transfers are done away. This is different from ACH payments, which are done in groups three times a day. When you do a wire transfer of money, it is sure to arrive on the day. On the other hand, ACH money can take a few days to actually come through. Wire transfers of money also cost more than ACH payments. The cost of wire transfers of money can be really high; sometimes they can cost the customers of wire transfers of money up to sixty dollars.

The choice between these two options really depends on what you need. If you have to send a lot of money and can’t wait, then a wire transfer is an idea even though it costs more. ACH is usually the choice if you are making regular payments or paying employees. This is because ACH is cheaper, and you can get your money back if something goes wrong with ACH. Also, ACH works with the systems you already use, like your bank. Wire transfers are an option when you need to send money, like when you’re in a hurry and need the money to arrive on the same day with wire transfers. For things, ACH payments are the way to go with ACH. Square

The relationship between ACH and EFT needs to be explained. EFT, which is short for electronic funds transfers is a term that includes all kinds of payments. So ACH and EFT payments are basically the thing because they use the same payment system. All ACH transactions are EFTs. However not all EFTs are ACH transactions. To understand this consider squares and rectangles. ACH transactions are like squares. EFT is, like rectangles. ACH transactions are a type of EFT. EFT includes types of electronic payments as well. ACH is a type of EFT and all ACH transactions are part of the EFT system. Square

Same-Day ACH: The Game Changer

The thing that is really exciting in the ACH world now is Same-Day ACH. Same-Day ACH is getting bigger and bigger. In 2024 the number of same-day ACH payments went up by 45 percent from the year. This is a deal because it means that Same-Day ACH was used for payments that were worth $3.2 trillion in total. Same-Day ACH is clearly something that businesses want to use because they want to be able to move their money. In the quarter of 2025, Same-Day ACH was used to settle 336.4 million payments. These same-day ACH payments were worth $980.3 billion. These numbers are not just big. They show that people are starting to think about payments in a way. Both businesses and people are starting to use Same-Day ACH because they want to be able to make Same-Day ACH payments. Same-Day ACH is changing the way we think about making payments with Same-Day ACH. Plaid

Same-day ACH transfers are a type of ACH transfer that works fast. They check the balance in your bank account on time. Settle payments quickly. These same-day ACH transfers happen in three batches every day. You have to send the money by 4:45 p.m. EST. It will not go through. As of 2026, you can send up to $1 million with same-day ACH transfers. This is a thing for businesses because they can now use same-day ACH transfers for big payments that used to require wire transfers, which are expensive. Same-day ACH transfers are getting to wire transfers in terms of speed, but same-day ACH transfers are still cheaper. For people who get paid by their employer, they usually send the money a day before payday. This way the money is in your account by 9 a.m. On the day you get paid. Same-day ACH transfers are making it easier for employers to pay their employees on time with same-day ACH transfers. StripeStripe

How Long Does an ACH Transfer Take?

People often ask about ACH. The answer to this question is that it depends on things. ACH transfers usually take one to three business days to complete. This is because the time it takes for an ACH transfer to go through can vary depending on when the transaction started and what time of day it is processed.

In the past, it would take ACH transfers around 3 to 5 business days to reach their destination. Now the ACH Network gives people options for how they want to process ACH credits. For example, people can choose to do same-day ACH transfers, next-day ACH transfers, or two-day ACH transfers.

The way the ACH Network works has changed a lot over time. Now people who start ACH transactions have a lot more options for ACH transfers than they used to. This means that people have a lot of flexibility when it comes to ACH transfers. The ACH Network and ACH transfers are more convenient than they used to be. Stripe

You have to keep in mind one thing about ACH transactions. ACH transactions only take place on business days. If you try to send money on a weekend or a holiday, it will not go through until the business day. The same thing happens if you send money in the day and the bank has already sent out the last batch of transactions. In that case, the money will not be credited to the account until the business day.

For instance, let us say you start an ACH transfer on a Friday afternoon after the bank has already sent out the batch of transactions for the day. The money might not actually be available in the account until Tuesday of the week if Monday is a holiday.

It is really important to think when you have to make payments that need to be made on time, such as ACH transactions for rent or loan payments. This way you can make sure that the ACH transactions go through when they are supposed to and you do not miss any payments, like rent or loan payments, through ACH transactions. PNC

Is ACH Safe? Understanding ACH Security

Security is a concern when we talk about sending money electronically. The good thing is that the ACH network has security in place at every step. Nachas rules include guidelines to prevent fraud and protect all the people involved. Like banks, credit unions, and companies that process payments. Have to follow these rules to be part of the network.

The way ACH transactions work is that they can take days to go through. This waiting time can be frustrating for people. It is actually a good thing. It gives the network time to watch out for transactions and look into them before the money is completely transferred. If something goes wrong, like sending money to the wrong person or the wrong amount, it is possible to reverse the payment and get the money back. This is usually only possible if there was a mistake. The fact that ACH transactions can be reversed is a security plus compared to wire transfers, where the money is gone for good once it is sent. So you need to be careful about who you allow to take money from your account because once you give a company permission to do so, they can keep taking money from your account. Consumer Financial Protection BureauPNC

ACH Fees: What Do Banks Actually Charge?

The cost of using ACH transactions is one of the reasons people like to use this way of paying instead of other methods like wire transfers or credit card payments. For people like you and me, a lot of ACH transactions do not cost anything. Your bank does not charge you to get your paycheck into your account. Most banks and credit unions also do not charge you to pay bills.

Your bank or credit union may have a limit on how much money you can move from one account to another. They may also charge you for each transaction. So it is always a good idea to check the rules of your account. Usually the fees for ACH transactions are very small compared to other ways of paying. Consumer Financial Protection Bureau

For businesses the numbers work out better. ACH payments are really cheap per transaction. They take 1 to 3 days to settle. On the other hand, wire transfers cost between $10 and $30 per transaction on average. When you are paying 500 employees or collecting fees from 10,000 customers, a $1 or $2 difference per transaction adds up to a lot of savings over a year. Many businesses choose ACH over credit card processing because it is more cost-efficient. Credit card interchange fees range from 1.5% to 3.5% of each transaction. For businesses with lots of payments ACH is the most affordable option in the US banking system. Businesses are choosing ACH payments more and more. ACH payments are a choice for businesses with many recurring payments. Plaid

Conclusion

The Automated Clearing House, which is also known as ACH, is very important to the financial system. It helps process a lot of money every year. This makes it possible for people to get their paychecks and for companies to get paid for things, like electricity. The Automated Clearing House also makes it easy for people to pay their bills automatically.

Understanding what the Automated Clearing House means is not something you know for fun. It is actually very useful to know what the Automated Clearing House is. This knowledge can help people manage their money better. It can also help people choose the way to pay for things. It can help people avoid paying extra fees they do not need to pay.

Whether you are a person trying to understand your bank statement or a business owner trying to find a way to handle payments, you should learn about the Automated Clearing House. The time you see the letters “ACH” on a transaction, you will know what is happening. Knowing about the Automated Clearing House is very helpful.

Frequently Asked Questions

1. What does ACH mean on my bank statement?

When you see “ACH” on your bank statement it means an electronic funds transfer happened through the Automated Clearing House network. This can be a payment you made which is called an ACH debit. It can be money that was put into your account, which is called an ACH credit. For example it could be your paycheck or a tax refund. The Automated Clearing House network helps move money between banks. It handles lots of transactions, at once. So ACH is just a way to show that money was moved electronically.

2. Can an ACH payment be reversed or cancelled?

Yes, ACH payments can be reversed. It happens only in certain situations. For example, if the wrong amount was. The wrong account was used, or it was a duplicate payment. The reversal has to be done usually within five business days. This is different from wire transfers. The fact that ACH payments can be reversed is a protection for consumers. It helps keep their money safe. ACH payments are often used for the deposit of paychecks and for bill payments. Reversing an ACH payment helps fix mistakes.

3. Is ACH the same as direct deposit?

Direct deposit is a type of transaction that uses the ACH network. It is called an ACH credit. All direct deposits go through the ACH network. The ACH network is used for other things too. For example, it is used for bill payments, which are also known as ACH debits. The ACH network is also used for tax payments and for people to send money to each other. Direct deposit and these other things all use the ACH network. The ACH network does a lot of things, including deposits.

4. What information do I need to send or receive an ACH payment?

To send or receive an ACH payment, you usually need the recipient’s bank routing number and their checking account number. Some platforms will also ask for the account holder’s name and what type of account it is, like a checking account or a savings account. You do not need a credit card or wire instructions to do this with an ACH payment.

5. How is ACH different from Zelle or PayPal?

Zelle and PayPal and Venmo are payment apps that people use. These apps may use the ACH network when money is moved to or from a bank account that is linked to the app. Zelle and PayPal also have their own way of moving money around for some transactions. The ACH network is like the behind-the-scenes system that makes things work. It is not something that people use directly. Zelle and PayPal are, like, the layer that people interact with. They use the ACH network and other systems to move money.