Table of Contents

CIBIL Score Range in India: Your Complete 2025 Guide to Understanding, Improving, and Mastering Your Credit

For CIBIL score range, imagine walking into a bank feeling confident and well-dressed and asking for a loan. The banker does not even look at your salary slip. They quietly type something into their computer. At that moment your entire financial history is being summed up in a three-digit number. That number is your CIBIL score range. It can. Open doors or shut them before you even have a chance to explain yourself. For millions of Indians every year, this score decides whether they can buy their dream home, start a business, or get a credit card that suits their lifestyle. Most people only have an idea of what the CIBIL score range means. Few people know how to improve their score on purpose. This guide aims to change that. It will explain everything thoroughly and honestly using language.

The Real Story Behind Your CIBIL Score

Your CIBIL score range is not something that banks have made to make things tough for you. It is actually a system that uses facts and numbers to find the answer to a question. This question is, if banks lend you money, will you pay it back? The CIBIL score is a three-digit number that shows how you have handled credit. This includes every payment you have made or missed. It includes every credit card bill you have paid or not paid on time. It also includes every loan application you have made. When you think about the CIBIL score in this way, it does not feel like someone is judging you. Instead, the CIBIL score feels like a tool that you can use and make better. You can really. Improve your CIBIL score. The CIBIL score is a tool that’s really about your credit behavior. Your credit behavior is what the CIBIL score is based on.

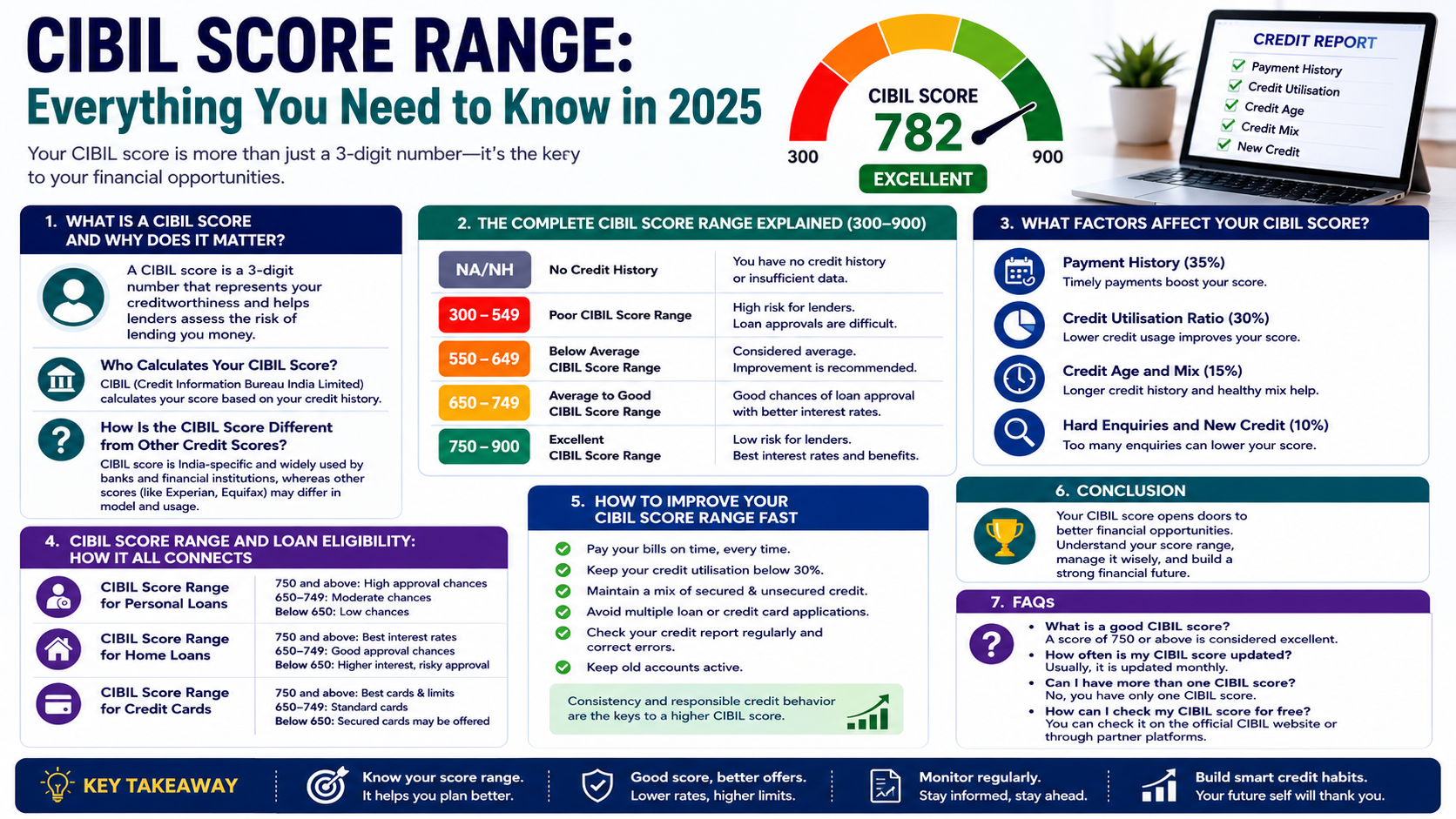

The scale goes from 300 to 900. When your credit score range is close to 900, lenders think you are good with money. You can get better deals. If your credit score range is above 750, it is very good. Most banks in India like to lend money to people with a credit score above 750 because they think these people are safe to lend to. They give them the interest rates and approve their loans quickly. It is important to know your credit score range and understand why it is what it is. This is the basis of making financial decisions when you are using credit. Your credit score is a part of your financial life.

What Makes CIBIL the King of Credit Bureaus in India?

India has four RBI-licensed credit bureaus: TransUnion CIBIL, Experian, Equifax, and CRIF High Mark. However, CIBIL is uniquely dominant in the market. It was incorporated in the year 2000 and, hence, is the oldest and most integrated credit bureau in India. Banks, NBFCs, housing finance companies, and online lending organizations make use of the data collected by CIBIL as their first preference while considering applications for loans. CIBIL uses the data that it collects from its members, which include practically all leading banks in India, and creates personal credit reports and scores. The score formula that CIBIL has devised based on over two decades’ worth of data on Indian borrowers has become incredibly accurate in predicting future repayment behavior. Whenever the banker speaks of your credit score, nine out of ten times, he or she is referring to your CIBIL score.

Why Your CIBIL Score Follows You Everywhere

And here’s another aspect of the CIBIL score range that many people realize too late in their lives—it is not just about loans anymore. The CIBIL score range has evolved into an all-encompassing metric that has now started to influence aspects outside of its original purview. Some employers, especially those in the financial industry, consider credit scores when conducting a background check prior to offering any job to someone. Many landlords who provide luxury properties for rent also consider credit scores while shortlisting potential tenants. And some insurance companies are even considering using credit information for underwriting.

Decoding Every Band of the CIBIL Score Range

Now let us discuss each range of the CIBIL score range one by one. The importance of comprehending the actual meaning of the bands of the score lies in the fact that only those who know about its significance are considered educated borrowers, while all others are surprised in front of the loan desk.

Score Range Category Loan Approval Odds Likely Interest Rate NA / NH No History Uncertain Lender Discretion 300 – 549 Poor, Very Unlikely, Very High (if approved) 550 – 649 Below AverageDifficultHigh650 – 749Average to GoodModerate to HighModerate750 – 900 Excellent Very High Best Available Rates

The Ghost Zone For CBIL — NA/NH Score

Prior to the scoring being done on a numbered scale, there is a class that does not fit into it at all—the one with scores NA (Not Applicable) or NH (No History). It means that you do not have a credit history at all. There was never any loan or any credit card in your life, and therefore, there was never a report submitted about your credit behavior to the bureau. In other words, you are literally invisible in the credit system, which might be quite paradoxical. As far as we know, credit cannot be built without having a credit history in the first place. On the other hand, you cannot have a credit history without taking any credit in the first place. The only possible solution would be a secured credit card with a fixed deposit that is extremely popular among people starting their credit life. Sometimes, even a small consumer durable loan can do the trick.

A score anywhere between 300 and 549 is a serious warning signal, and anyone in this range needs to treat it as such. This range almost always reflects a history of genuine credit problems—loan defaults, accounts sent to collections, repeated late payments, or credit card settlements where the full outstanding amount was not repaid. Lenders look at this range and see a borrower who has demonstrably struggled to manage borrowed money in the past, and most mainstream banks will decline applications outright rather than take the risk. This doesn’t mean you’re financially doomed — it means you have significant ground to make up, and that requires patience. The journey from 400 to 600 is not quick, but it absolutely happens for people who commit to paying every single bill on time, reducing their outstanding balances, and staying away from new credit applications while their record has time to heal.

The Struggle Zone — 550 to 649

A credit score range of 550 to 649 would best be described as mediocre when it comes to finance, not terrible enough to lead to immediate rejection but certainly not good enough to give you much leeway. While you may receive loan approvals from NBFCs and some online lending portals, you would have to pay much more interest on them than borrowers with better scores. To put this into perspective, a borrower with a credit score of 780 will get a personal loan at an interest rate of 12%, while a borrower with a 620 score could end up paying 16% or 17% for the same loan. Considering that you would need to pay around ₹5 lakh in loan installments for a period of three years, you can imagine how much of a difference even a few percentage points in interest rates make. This particular range of scores is extremely flexible and is relatively easy to improve with a few months of good behavior.

It’s time to enter the area where things begin to improve. A credit score range in the range from 650 to 749 indicates that you are a responsible and reputable borrower. You can apply for a personal loan, a car loan, and a credit card with relative ease, although the best interest rates might still not be available, since they are reserved only for borrowers whose scores exceed 750. Imagine this zone as a business class seat on an airplane: comfortable and luxurious enough, certainly better than the rest, yet not as prestigious as first class. The great thing about this particular zone is that you’re very close to achieving even better scores. It takes little time to move from 720 to 760, which can be achieved in several months with some effort — for example, paying off your debts and making sure no late payments follow.

The Winner’s Zone — 750 to 900

Above 750 is where the true advantages of good credit behavior start paying off in concrete and quantifiable terms. Lenders are actively looking to make loans to individuals in this category, as statistics show they are trustworthy borrowers. There is quick approval for loans, the best interest rates are offered, and lenders may even make offers before being approached. Credit cards with premium benefits like airport lounges, high rewards points, and generous cashbacks become accessible to you. You have significantly more leverage; you can visit a lender with a counteroffer and ask them to match or beat it, and they usually do. The top of the chart is occupied by 900, and this number is exceedingly rare. Maintaining a 900 demands impeccable credit behavior, such as timely repayments, a low credit utilization ratio, a lengthy credit history, and fewer credit inquiries. It is commonly agreed upon by financial experts that although maintaining a 900 is commendable, a 750 gets you access to everything the Indian credit market has to offer.

The Hidden Forces That Shape Your CIBIL Score Range

Your score doesn’t go up or down at random. Each shift in your credit score range reflects certain behaviors that the credit reporting agency’s formula is subtly tracking. The following are the most important factors to be aware of.

Your Repayment Track Record

If credit scores were buildings, your payment history would be the base of those structures. There is no more important element than your payment history in deciding what place your credit score holds. Each EMI paid on time gives a silent boost to your credit score. On the contrary, missing an EMI – even if just by a few days – leaves a dark mark on your credit score report, which remains there for several years after the default. Lenders are mostly concerned about the repayment history in the last one or two years. So if you had a troubled repayment history three or four years back but have been making your payments on time since then, you can improve your credit score over time. The most effective step you can take to improve your credit score is to automate each payment.

The 30% Credit Utilization Rule Nobody Told You About

The credit utilization rate of yours is the percentage of your overall authorized credit limit that you have currently used, and its significance cannot be overstated. If your total credit card limit across all your cards amounts to ₹200,000 and the current amount on which you’re running a debt equals ₹120,000, then your credit utilization ratio equals 60%. This number might seem alarmingly high to the credit bureau. The general rule of thumb is not to exceed 30% of your total credit limit at any point in time. By going above this level, you send the signal to the bureau that you are probably under financial pressure despite being able to meet your payment obligations in full and on time. Fortunately, there is a smart trick that financially literate Indians play to reduce their credit utilization rate: ask for a credit limit increase from time to time.

The Age and Variety of Your Credit Portfolio

There are two aspects that operate under the radar but have a significant impact on your score, and these are the age of your credit accounts and the variety of your credit mix. The older your credit accounts are, provided that they are all in good standing, the more beneficial their presence will be for your score. This is why canceling the old credit card account that you don’t use anymore could be an ill-conceived decision since even if the card is lying dormant in your closet, it’s working hard on your behalf by adding to your credit age and your overall credit limit. Regarding credit mix variety, the ability to handle both secured and unsecured loans is essential because it indicates to lenders that you’re able to manage various financial products wisely, and this is what the algorithm appreciates.

Hard Enquiries — The Silent Score Killers

Each time you fill out an application form for a loan or a credit card, the institution checks your CIBIL report and determines your suitability to receive credit. This type of activity is referred to as hard inquiry, and each one affects your score slightly. One hard inquiry does not hurt your score much; however, several applications in a relatively short period can be detrimental. For instance, if you apply for three personal loans and two credit cards within a month, you end up with a batch of five hard inquiries, which will make you appear as a borrower who desperately needs credit, which will not work well for you. The recommended strategy would be to conduct adequate research on different products available and select the best fit based on your profile.

CIBIL Score Range and What It Unlocks for You

Knowing about your credit score in theory is one thing, but the real question is: what exactly does this score give me? Take a look at how various score bands affect different financial products available in India.

Personal Loans and Your Score

This is because personal loans are not collateralized in any form whatsoever. There is no security offered by way of property, assets, or otherwise; just the borrower’s word that they will repay the debt. For this reason, the criteria set for the credit score requirement of personal loans tend to be strict. The standard for personal loans should ideally lie somewhere around 750 points or more in order to be eligible for a loan. However, even a credit score in the range of 700–749 would be considered suitable for a personal loan. Nonetheless, you would have to pay a higher interest rate than those who have a 750 or more credit score. A personal loan becomes almost impossible to procure if your credit score is less than 700 unless you approach an NBFC or consider taking out a secured loan.

Home Loans — Where Your Score Saves You Lakhs

It is safe to say that a housing loan is the biggest investment an Indian makes in his or her lifetime, and any slight difference in the rate of interest would mean lakhs of rupees saved or lost over a period of two decades. Lenders are relatively flexible when it comes to housing loans compared to personal loans because the asset that is bought becomes the security in case of default. This means that housing finance companies will be willing to take risks and approve applicants who have a credit score range as low as 680 or 700, provided that other factors such as income and occupation are stable. Nonetheless, the perfect score range where an applicant can bargain between different lending institutions and compare interest rates is still much higher at around 750. It may be possible to cut down ₹10–15 lakhs in interest by increasing your score to 780 or 800 prior to applying for a housing loan.

Credit Cards — From Basic to Premium

The credit card industry in India has seen a boom in the recent past, offering everything from the basic cards to premium cards made of metal with excellent benefits during travel. Your CIBIL score range is the key determinant of what kind of credit card products you are eligible for. Cards such as the basic and secured cards will be available to individuals with CIBIL scores even less than 700 and even those without any credit history, as these are the cards meant to improve your CIBIL score range. Reward points and cash-back cards are available to those whose CIBIL score range lies between 700 and 750. Premium cards issued by the top banks, offering lounge access in airports, high reward points, and concierge service, require scores more than 750 and steady income proof.

A Practical Roadmap to Push Your CIBIL Score Range Higher

Enhancing your CIBIL score range is not rocket science; however, it requires discipline over the long haul. Just think about health and fitness; everybody knows what needs to be done, but the people who benefit are the ones who show up every day compared to the ones who run hard for seven days and then stop. Below is a realistic guide for how to do it.

First, make sure to pay your dues in full and without fail. Schedule automatic deductions for every loan repayment or credit card bill to eliminate the possibility of any late payments. You might find yourself in financial trouble during some month, but try to pay something towards your credit card bills even if you have to pay the minimum required. The second thing that will improve your score rapidly is reducing your credit utilization ratio to less than 30 percent. If your ratios are currently above that level, work on reducing them to as low as 35 percent or even lower if possible. Finally, avoid applying for many loans or credit cards simultaneously or at the same time.

With regard to strategies, one might consider applying for a higher credit limit on the credit cards issued by the current lenders; this will bring down your utilization ratio without having to make additional purchases. One should look at his/her CIBIL report at least three times a year to correct errors if there are any because such errors are very frequent and affect the borrower’s score adversely. Lastly, if one is beginning his/her credit career with an NA/NH credit score, one should start by using a secured credit card or taking a small consumer durable loan, which can then be used diligently for building up an impeccable credit record.

Common CIBIL Score Range Myths That Are Costing You

There are several misconceptions regarding CIBIL scores that you may find difficult to believe. However, it is essential to understand the truth since acting on incorrect information will not only fail to help but also hurt your CIBIL score.

Myth 1: Checking your own CIBIL score hurts it. This is entirely untrue. When you check your own score, it is categorized as a soft inquiry and does absolutely nothing to affect your score. On the contrary, checking it frequently is possibly one of the most financially prudent decisions that you can make, since it helps you identify mistakes and gauge your progress.

Myth 2: A higher salary leads to a higher CIBIL score. Your salary has absolutely nothing to do with how your CIBIL score is calculated. Your CIBIL score range consists entirely of your past credit behavior – whether that includes payment history, utilization, credit age, or any other form of inquiry. Someone who earns ₹10 lakhs per month but pays their bills late would have a very poor score, whereas an individual who earns only ₹30,000 per month and handles their finances carefully would have a great score.

Myth 3: Canceling old credit cards helps raise your score. As previously stated, the opposite is true. Canceling old credit cards lowers your credit history and total credit limits, making your score lower. In most cases, it is better to keep old credit cards open because there may be legitimate reasons for this action.

Myth 4: It is equivalent to repaying a debt if you settle a loan. Loan settlement, where the creditor agrees to settle the loan at an amount lower than the debt, will show up in your credit report under “settlement” status instead of “closure.” If possible, pay off your loans in full.

Conclusion

The CIBIL score range is such an idea that appears straightforward yet holds much importance in practical matters. It is only a score from 300 to 900 but comes with much importance to your financial life, your credit score range, and the way you can acquire homes and cars as well as other financial opportunities through the exercise of your choices. Indeed, this score is completely under your own power, as it will depend greatly on the actions you take regarding money management. If you pay your bills punctually and wisely use your credit card and build your credit history and look through your report for possible mistakes, your score will improve without any doubts since this system encourages exactly this kind of behavior.

Frequently Asked Questions (FAQs)

1. What is the ideal CIBIL score range to get a home loan at the best interest rate?

Scores of 750 and higher fall within the ideal range for mortgage applications. Lenders tend to provide the lowest rates to those who fall within this range. Scores higher than 780 provide good bargaining power with several lenders, allowing one to save a lot of money in the process.

2. How quickly can I improve my CIBIL score range from 600 to 750?

Through diligent efforts such as timely payments, minimizing credit utilization, and avoiding additional hard inquiries, you can expect to see significant progress in about 12 to 18 months. The time frame will vary based on how bad your report is.

3. Will closing a credit card I never use help my CIBIL score?

No, generally not. Cancellation of an existing card means lowering the amount of your credit limit as well as the length of your credit history, which will affect your score negatively. Unless you’re paying a very expensive annual fee for the card without any perks, it’s best to leave the account open and use it occasionally.

4. Can I get a loan if my CIBIL score range shows NA or NH?

Yes, but your choices will be fewer. There are some banks that offer you secured credit services like fixed deposit loans or secured credit cards for individuals who do not have any credit history. This is a wonderful way to build your score from the ground up.

5. How often does my CIBIL score range get updated?

The update of your CIBIL score range depends on how often your lenders provide information to the bureau regarding your credit behavior; usually, it happens after a period of 30 to 45 days. It implies that any improvement in your credit behavior, such as paying back outstanding debts, will be reflected in your CIBIL score within a month or two.