Table of Contents

How to Improve Your CIBIL Score: The Complete 2026 Guide

Let us be real. There is nothing more frustrating than walking into a bank with confidence, asking for a loan, and getting turned down because of your CIBIL score. Your CIBIL score is a three-digit number. It has a lot of power over your ability to borrow money in India. Whether you want a home, a car, or a better credit card, your CIBIL score is like a gatekeeper that decides if you can have these things. The good thing is that having a CIBIL score is not forever. You can make it better. This guide will show you how to do it.

Think of your CIBIL score like a report on how you handle money. Every time you pay a bill late or use up all the money on your credit card, it gets noted down. You can change this by being more careful and consistent. Most banks in India think a CIBIL score of 750 or more is good for getting a loan. You can get to this score in about six to twelve months if you try hard and do the right things. Your CIBIL score is important. It is worth taking care of. You can improve your CIBIL score. Get the things you want. Credit Guide India

What Exactly Is a CIBIL Score and Why Does It Matter?

Before we dive into the details, let’s be clear about what a CIBIL score is. A CIBIL score is a 3-digit number that shows your credit history. It is given by TransUnion CIBIL. The CIBIL score ranges from 300 to 900. A higher CIBIL score means you have chances of getting a loan approved.

But a CIBIL score is not any number. It is a summary of all your financial decisions involving borrowed money. Every EMI you paid on time, every credit card bill you paid or ignored, and every loan you applied for. It all affects your CIBIL score. Lenders use this CIBIL score to decide about giving you a loan. Whizseed

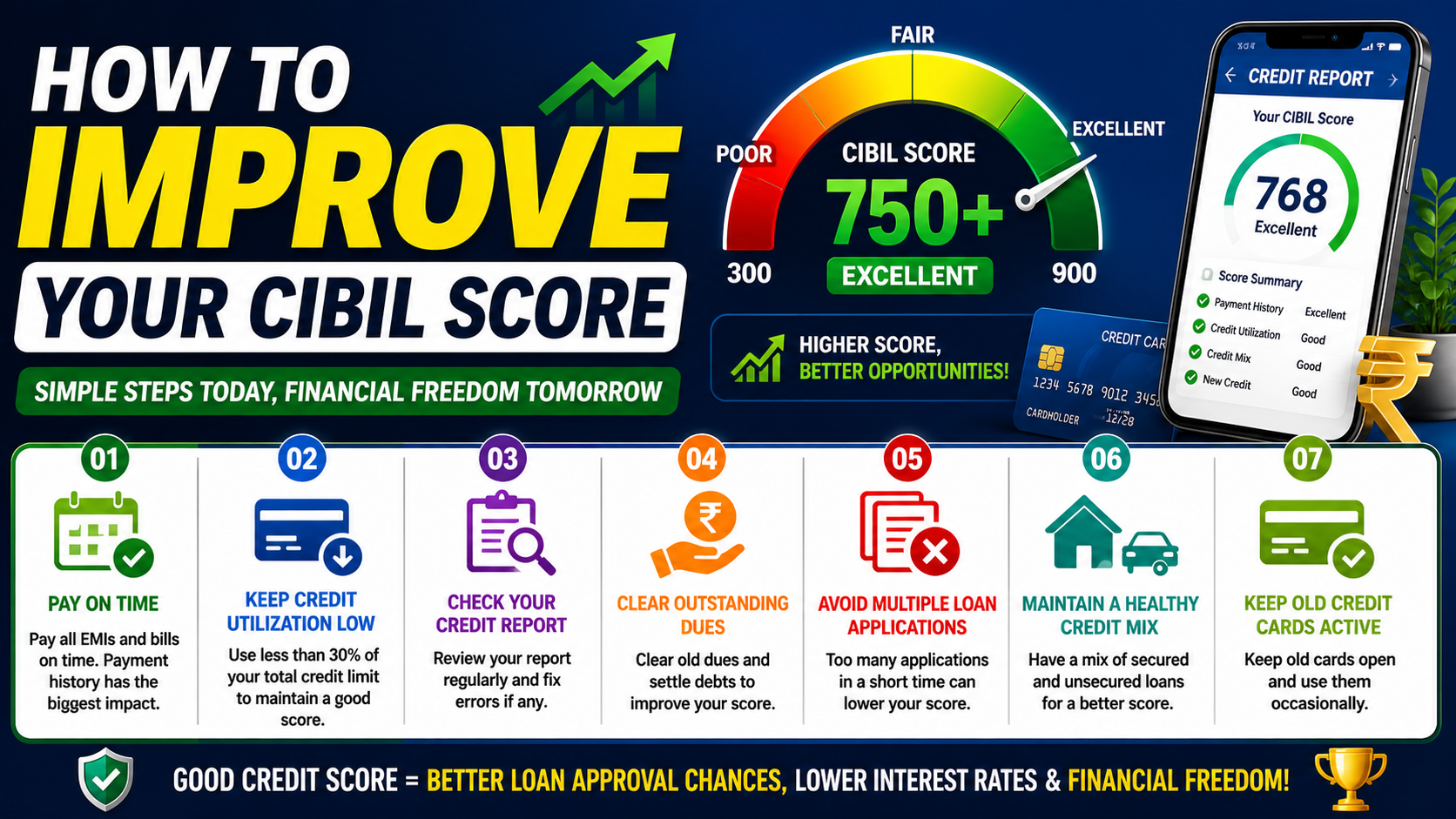

The CIBIL Score Range Explained

Understanding your CIBIL score helps you set goals. Your CIBIL score can range from 300 to 900. The closer your score is to 900, the better it is. A CIBIL score between 300 and 549 is considered poor. On the other hand, a score from 550 to 700 is fair. A good CIBIL score is above 750; that’s what you should aim for. If your score is around 600, do not worry; you are in the zone. With a plan to improve, you can get a score in a few months. You can push your score into the territory. Bajaj Finserv

| Score Range | Category | What It Means |

|---|---|---|

| 300 – 549 | Poor | High risk; most lenders will reject |

| 550 – 649 | Fair | Limited options; higher interest rates |

| 650 – 749 | Good | Decent approval chances |

| 750 – 900 | Excellent | Best rates and faster approvals |

How Your CIBIL Score Affects Your Financial Life

This is where things get really interesting. And to be honest, a little surprising. Your CIBIL score affects your life in several important ways: A high CIBIL score helps you get a loan approved. A good CIBIL score helps you get loans at lower interest rates, and a strong CIBIL score may help you get higher credit limits on credit cards and loans. The effect of a CIBIL score goes beyond just getting a loan approved. If you have a CIBIL score of 800 or above, you can get an interest rate on your home loan of 0.25-0.50%, which means you can save a lot of money over a 20-year loan period. Think about this for a moment. Improving your CIBIL score could save you a lot of money over the lifetime of a home loan. If this is not enough, many banks and financial companies now check CIBIL scores when they hire people, and non-banking financial companies and fintech companies always check credit scores before hiring. Especially for jobs that involve handling money or client accounts. So yes, your CIBIL score can even affect your career in 2026. Federal Bank + 2

What Causes a Low CIBIL Score?

You cannot fix a problem if you do not understand it. So before we try to make things better, we should take time to see what is making your CIBIL score low. Your payment history and credit utilization ratio are very important. These two things make up more than 60 percent of your CIBIL score. This means that most of your CIBIL score is based on how you pay your bills and how much of your credit you are using.

When you know this, it is easier to see how to make your CIBIL score better. Your CIBIL score is like a report card, for your credit and payment history and credit utilization ratio are the things that affect your CIBIL score. Intensify

Common Mistakes That Damage Your Score

People often hurt their credit scores without even realizing it. There are things that can make your CIBIL score low. For example, paying bills all the time, using too much of your available credit, applying for too many loans or credit cards, and only having one type of credit. Some people also make a mistake when they close old credit card accounts. When you do this, you have credit available, and your credit history gets shorter. Both of these things are bad for your credit score. Using up all your credit limit is not a good idea because it looks like you really need credit to get by. Applying for a lot of loans at the time can also hurt your credit score. These are not financial mistakes; they are just things people do every day that slowly hurt their creditworthiness over time. The credit score gets hurt by things like payments on your credit cards and loans; high credit utilization on your credit cards; multiple credit inquiries when you apply for many loans or credit cards; and lack of credit mix when you only have one type of credit, like a credit card or a loan. These things can all make your CIBIL score low. Federal BankWhiz

If you miss a payment, your credit score can go down by 50 to 100 points. This is a lot of damage from something that might seem like a mistake. The credit bureaus will mark your account as delinquent. Once this mark is on your record, it will take a time, many months of doing everything right, to fix the damage. So it is really important to know why these things happen. Understanding the reasons for a CIBIL score is not just about learning something new; it is the basis for making your CIBIL score better. Intensify

How to Improve Your CIBIL Score: Step-by-Step Strategies

Now we are getting to the heart of the CIBIL score. These are not tips that you can find on old financial blogs. The CIBIL score is what matters here. These are. Practical strategies that directly talk about the factors that CIBIL weighs most heavily when it comes to the CIBIL score. You can think of each strategy as a lever that can help your CIBIL score. If you pull enough of these levers in the direction, your CIBIL score will start to climb up.

1. Pay Your EMIs and Bills on Time — Every Single Time

If you remember one thing from this article, remember to pay everything on time. Paying on time is the important thing for your CIBIL score. It is 35 percent of your score. When you pay late, it is a problem. This happens with things like loan payments or credit card bills. It is simple: if you do not pay on time, your credit score will not be good. It does not matter if you use your credit a little or if you have accounts. If you miss payments, your CIBIL score will be bad.

The easiest way to fix this is to set up payments for your loan payments and credit card bills. You can pay more if you want. Automatic payments mean you will never miss a payment. If you pay on time, your CIBIL score will get better in 30 to 45 days. If you make three payments on time in a row, your CIBIL score can go up by 30 to 50 points. Start paying on time today. You will see a difference in your first billing period. Paying on time is the key to a CIBIL score. Your CIBIL score will thank you if you pay everything on time. InvsifyInvsify

2. Keep Your Credit Utilization Below 30%

Your credit utilization is the biggest thing that affects your score. It is also one of the ways to make your score better. The credit utilization ratio is like a report card for how much of your credit limit you are using. If you use a lot of your credit limit, it looks bad to lenders. They think you are desperate even if you pay your bills on time. If you keep your credit usage below thirty percent, it shows that you are responsible with money. This helps your score get better fast. For example, if your credit card has a limit of ₹100,000, you should try to spend no more than ₹30,000 on it each month. If you want a great score of 800 or more, try to keep your credit utilization below ten percent. If you always use a lot of your credit limit, you can ask your bank to increase your limit. This will make your utilization percentage go down. You will not have to spend less money. This is a smart thing to do that a lot of people do not think about. If you get a credit limit and do not spend more money, your credit utilization ratio will go down. This is one of the ways to make your score better without changing how you live your life. Your credit utilization will get better. So will your credit score. InvsifyBeincareer

3. Check and Fix Errors in Your Credit Report

This is probably the forgotten way to improve your CIBIL score, and it can give you really fast results. A lot of people do not check their credit report for years thinking it is correct. Mistakes happen more often than you think. When you check your report, look for any mistakes. These mistakes can be information about your loans you do not know about, wrong payment history, or duplicate entries. Even small mistakes can lower your CIBIL score. If you find any mistake, tell CIBIL about it on their website or app. Fixing these mistakes can help improve your CIBIL score. The process of fixing mistakes is actually quite easy. Go to the CIBIL website and find the Dispute Centre to report the mistake. Tell them what is wrong and add any documents you need to prove it. The lender has 30 days to check and respond. If they find the mistake, CIBIL will fix it. Update your CIBIL score. It is like finding money you did not know you had. Some people have seen their CIBIL score go up by 20 to 40 points by fixing mistakes in their report without changing anything else about their money. Whizseed My Mudra

4. Clear Outstanding Dues and Settle Old Debts

Outstanding debts are like financial anchors dragging your score to the bottom. Debt weighs down your CIBIL score faster than most other factors. Multiple unpaid loans or high-interest credit card balances signal financial stress to credit bureaus, dragging your score into the danger zone. Clearing high-interest debts first frees up cash flow, which you can then redirect toward other dues. If you have multiple debts, prioritize them strategically rather than trying to tackle everything at once. Attack credit cards and personal loans first since they typically carry the highest interest rates. Once those are cleared, your credit utilization drops and your payment history improves simultaneously — a double win. If you have settlements and overdue accounts, these reduce creditworthiness. If possible, negotiate with the lender and aim for a “closed” status after full payment. A “settled” account looks better than an outstanding one, but a “closed” account (fully paid) looks best of all to future lenders. InvesifyCredit Guide India

5. Avoid Multiple Loan Applications in a Short Period

Debts are like weights that hold you back and hurt your credit score. The more debt you have, the more it hurts your CIBIL score. When you have a lot of loans or credit card bills with high interest, it tells the people who check credit that you are having money problems, and that pulls your score down. If you pay off the debts with interest first, you will have more money to use for other things you owe. Do not try to pay off all your debts at one time. That can be much. Instead pay off your credit card debt and personal loans first because they usually have the highest interest rates. When you pay off these debts, you will have money, and your credit score will get better. If you have debts that you have not paid and you have made a deal with the lender, try to get them to say that your account is closed after you pay the debt. This looks good to the people who lend money because it shows that you paid your debt and closed your account. A closed account is better than a debt that you have made a deal on. It is also better than a debt that you still owe. IIFL Finance Credit Guide India

6. Maintain a Healthy Credit Mix

Your credit portfolio is like food for your money. You need a bit of everything to be healthy. This means you should have some secured credit and some unsecured credit. Secured credit is like a home loan or a car loan. Unsecured credit is like a credit card or a personal loan. Do not take a loan just to have a kind of credit. This is not an idea. What is important is that you pay your bills on time and do not use much credit. If you only have credit cards, it might be an idea to get a small personal loan that you can pay back responsibly. This will add some variety to your credit profile. There are things that can affect your credit score. The two most important things are paying your bills on time and not using too much credit. These are the things you should focus on first. Once you have these under control, you can think about getting kinds of credit. A good credit mix is helpful. It is not as important as paying your bills on time and not using too much credit. So remember your credit portfolio is like your money’s food. You need to take care of it and make sure it is healthy. This means paying your bills on time and not using much credit. If you do these things, you will have a credit score, and you can get the credit you need when you need it. Credit Guide: IndiaBankBazaar

7. Keep Old Credit Cards Active

This is one of those things that people do not expect to hear. A lot of people think that closing credit cards you do not use is an idea when it comes to money. But they are actually hurting their credit scores by doing this. If you have credit cards, you should keep them as long as you can pay your bills on time and in full. This will help you build a credit history that is long and strong, and this will help you have a good credit score now and in the future. The length of your credit history is part of your CIBIL score. Having old credit cards is good for this. If you close them, you will have a credit history and a lower total credit limit. And this will make your credit score go down. The best thing to do is to use your credit cards for small things you buy every month like a subscription or a bill and pay them off in full every month. This keeps your account open. Helps you build a good record of paying on time without getting into debt. You should keep using your credit cards and pay them off every month to build a good credit history and a good CIBIL score. Bajaj Finserv

How Long Does It Take to Improve Your CIBIL Score?

The question that everyone wants to know the answer to is this: how long does it take to improve a credit score? The answer to this question is that it depends on the person and their credit score. The good news is that it does not take as long as you think it will. Usually it takes around four months to one year to improve a credit score. This is because it depends on the problems you had in the past and if you are doing things with your credit now. If you pay your bills on time and do not use much of your credit, then your credit score will get better. It also helps if you do not get much new credit. The time it takes to improve your credit score is different for everyone. It depends on how bad your credit score is and what is causing the problems. If you had a problem with using much of your credit, you can see your credit score get better in just one month. If you missed payments or did something really bad with your credit, it will take longer to make it better. A credit score is, like, it takes time to improve. If you do good things with your credit, like timely payments and low credit utilization, then your credit score will get better over time. BankBazaar

A Realistic Timeline for Score Recovery

The CIBIL score gets updated every thirty to forty-five days. If you start working on your CIBIL score today, you will see a difference in three to four months, and your CIBIL score will be seven fifty or more in six months. This is if you do not have any problems like defaults or settlements in your history. If your report has settlements or written-off accounts, it will take twelve to eighteen months to see an improvement in your CIBIL score. It may seem like a long time, but think about it like this: in twelve months your CIBIL score will be much better, or it will still be the same. The clock starts when you take action on your CIBIL score. You can check your CIBIL score as many times as you want, and it will not affect your CIBIL score. This is because checking your CIBIL score is a soft inquiry. Only hard inquiries, which are done by lenders when you apply for a loan or credit card, can reduce your CIBIL score. So you can check your CIBIL score using tools like CIBIL.com, Paytm, CRED, or BankBazaar as often as you like. Beincareer + 2

Common Myths About CIBIL Score Improvement

The internet has a lot of information about credit scores. If you believe the things, it can actually hurt your progress. Let’s talk about some of the common myths that stop people from making real progress with their credit scores. The first big myth is that closing credit cards is good for your credit score. This is actually not true. Closing unused credit cards can really hurt your credit score.

Some people also think that checking your credit report is bad for your credit score. This is not true at all. If you do not check your credit report, you might miss some mistakes that are hurting your credit score without you even knowing.

Many people believe that if you get turned down for a loan, it does not affect your credit score. When you get turned down for a loan, the loan rejection itself does not show up on your credit report. Before the bank says no, they do a hard inquiry, which does get recorded. So even though you do not see the loan rejection, you do see the hard inquiry, and a lot of inquiries in a short time can really hurt your credit score.

There is also a myth that you can improve your credit score fast, with some kind of trick. There is no real way to make your credit score better overnight. The steps we talked about are the way to safely improve your credit score. It is better to be consistent than to look for fixes. If someone promises to fix your credit score for a fee, they are probably trying to scam you. You should stick with the methods that we talked about. Consistency is what matters when it comes to credit scores. Credit scores are important. You should take care of your credit scores by using the right methods. IIFL Finance Credit Guide India

Conclusion

Improving your CIBIL score is not that hard; it just needs you to be disciplined and patient. You also need to know what the CIBIL score is about. To get a CIBIL score, you have to make a lot of small decisions every day. You have to pay your EMI on time. You have to not use much of your credit card. You have to check your report to see if there are any mistakes. You have to keep your accounts open. These things may not be very exciting. They show that you are good, with money. This is what you want your credit report to show about you. Improving your CIBIL score takes time. You have to keep doing the things to have a good credit profile. If you are patient and make choices with your money, you can get better deals, lower interest rates, and have more freedom with your money. So start working on your CIBIL score today and keep at it. Let time take care of the rest. Federal Bank

Frequently Asked Questions (FAQs)

1. Can I improve my CIBIL score from 600 to 750 in six months?

Yes, it is absolutely possible for most people to do this. The main things you need to do are pay off any debts, keep the amount you owe on credit below thirty percent, pay all your loan payments on time, and fix any mistakes in your credit report. Because CIBIL updates credit scores every thirty to forty-five days, doing the things for six months will usually make a big difference. But the results can be different for you depending on your credit history.

2. Does paying only the minimum due on my credit card hurt my CIBIL score?

Paying the minimum amount is a thing because it means you will not have to pay extra money for being late. It also means you will not get a mark on your credit report. This is good.

3. How often should I check my CIBIL score?

You should check your credit score at once every three months. Checking your credit score is a soft inquiry, and it has zero impact on your credit score, so there is no downside to monitoring your credit score regularly.

4. Will taking a new loan help improve my CIBIL score faster?

That is not always the case. A good mix of credit is a thing, but when you get a new loan, it can hurt your credit score for a little while. This is because it is like a check on your credit history. Also, you will have debt, which means you have to pay more money back. You should try to handle the credit you already have in a way. Getting a loan can be helpful, but only after you have a good handle on your current credit. It should not be the way you try to improve your credit.

5. What happens to my CIBIL score after a loan settlement?

When you settle a loan, you pay less than what you owe after talking to the people you owe money to. This is not the same as paying back the loan, which looks a lot better on your record because it says “closed.” Settling a loan can make it seem like you are having money problems. It can take a long time, like a year or more, to show that you are responsible with money again. If you are having trouble paying your debts, try to work out a plan to pay back the loan instead of settling because that is usually a better idea.